By Coral Gables Gazette staff

Coral Gables is collecting more revenue than last year. It is also falling behind.

At the midpoint of fiscal year 2026, the city had brought in $199.9 million — 71.9 percent of its annual budget. That is slightly below last year’s pace of 73.2 percent, even as the total budget has expanded by more than $16 million year over year.

The gap is modest in percentage terms. It is more revealing in structure.

A widening gap between expectations and activity

The most consequential signal appears in construction permits, one of the city’s clearest measures of development activity.

Through March, Coral Gables collected $7.1 million in construction permit revenue — about $958,000 less than at the same point last year, despite a higher annual target. Collections are running at 55.4 percent of budget, compared with 75 percent last year.

This is not simply a missed projection. It reflects a divergence between budget assumptions and collections to date. The city increased its construction permit revenue target by nearly $2 million year over year. At midyear, collections have not supported that assumption.

Planning and Zoning fees reinforce the pattern at a smaller scale. Collections stand at $4,341 — just 4.3 percent of budget. Even after a two-thirds reduction in the budgeted amount, revenue remains far below pace.

Together, the two categories suggest a slowdown in activity entering, or moving through, city review.

That matters because the timing coincides with broader commission concern over projects that may move through county approval processes rather than the city’s own zoning system. The financial report does not indicate whether any specific project bypassed city review or whether county routing caused the permit and planning fee shortfall. It shows only what the city collected. Still, the decline in those categories gives fiscal context to a policy concern commissioners have been raising: when development activity shifts outside city-controlled review, the effects may extend beyond planning authority to revenue.

An uneven development signal

Not all development-related indicators point in the same direction.

Board of Architects fees — tied to design review and project refinement — have nearly doubled year over year, reaching $956,650 at midyear, or 87 percent of the annual budget. At the same point last year, collections stood at $493,045.

The contrast is striking. Design activity appears strong. Permit revenue, which reflects construction-stage activity, is lagging.

One interpretation is that projects are advancing through review but not converting to construction at the same pace. Another is that a smaller number of projects are generating higher-value review activity without broad-based volume. The report highlights the disconnect.

Stable foundations, but limited upside

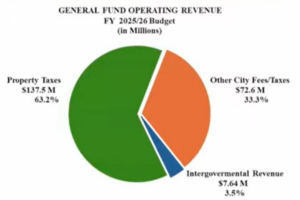

The city’s largest revenue source — property taxes — remains stable and predictable. Collections are slightly below last year’s pace but largely front-loaded, reflecting a tax calendar in which most collections arrive early in the fiscal year.

That stability carries a constraint. Property taxes anchor the budget. They do not expand midyear to offset weakness elsewhere. When variable revenue categories soften, the city has limited ability to recover within the same fiscal cycle.

This places greater weight on development-related revenue to meet budget expectations. It is precisely that category that is underperforming.

Rising costs in city-supported operations

While revenue shows uneven growth, several city-supported operations are moving in the opposite direction.

The Coral Gables Country Club fund required a $1.4 million transfer from the General Fund at midyear — nearly triple last year’s $507,400 transfer. The Transportation and Trolley fund posted a $1.4 million operating loss, wider than the prior year, with a $931,769 transfer from the General Fund.

These figures reflect policy choices. The city is maintaining or expanding recreation, mobility and other public services even as some revenue streams soften. The gap is absorbed through General Fund support.

That approach depends on recovery in underlying revenues, sufficient reserves, or future budget adjustments.

The Country Club figure arrives with particular timing. As the city debates pricing, access and use of public recreation facilities, the midyear report adds a fiscal dimension: the Country Club fund required $875,000 more in General Fund support than it did at this point last year. That context belongs in any discussion about who benefits from access, how prices are set and how much the broader tax base should subsidize the facility.

A budget built on growth assumptions

The fiscal year 2026 budget reflects a 6.4 percent increase over the prior year. Growth at that level implies confidence in fee generation, continued service demand and development activity.

At midyear, the data presents a more complicated picture. Some categories are outperforming: business licenses and alarm permits have already exceeded their annual targets. Others are significantly behind.

The shortfall is concentrated. That concentration matters. It points less to general economic weakness than to sector-specific deceleration, especially in construction-related activity.

It also arrives amid broader uncertainty over local-government revenue in Florida. Recent state discussions about reducing or restructuring property taxes remain unresolved, and any future change would directly affect the largest single revenue source for cities such as Coral Gables. The current report does show why the question matters: a budget already relying on growth-sensitive revenues would have less room to absorb a structural change in property-tax collections.

The second half becomes decisive

The remaining months of the fiscal year will determine whether the current gap is temporary or structural. Construction permit revenue can accelerate if projects move forward. Planning and Zoning activity can recover if new applications enter the city pipeline. Venetian Pool revenue should also strengthen after a partial-year reopening following renovation.

Each of those outcomes depends on conditions the city only partly controls.

The city’s financial position remains stable. Revenues are substantial. Core services are funded. What has changed is the alignment between growth expectations and underlying activity.

Coral Gables has built a budget that anticipates continued expansion. The first half of the year suggests that expansion is becoming less predictable.

That is a shift. And it raises a question that will shape the second half of the fiscal year and beyond: whether the city’s revenue model is keeping pace with the conditions it depends on — or beginning to diverge from them.